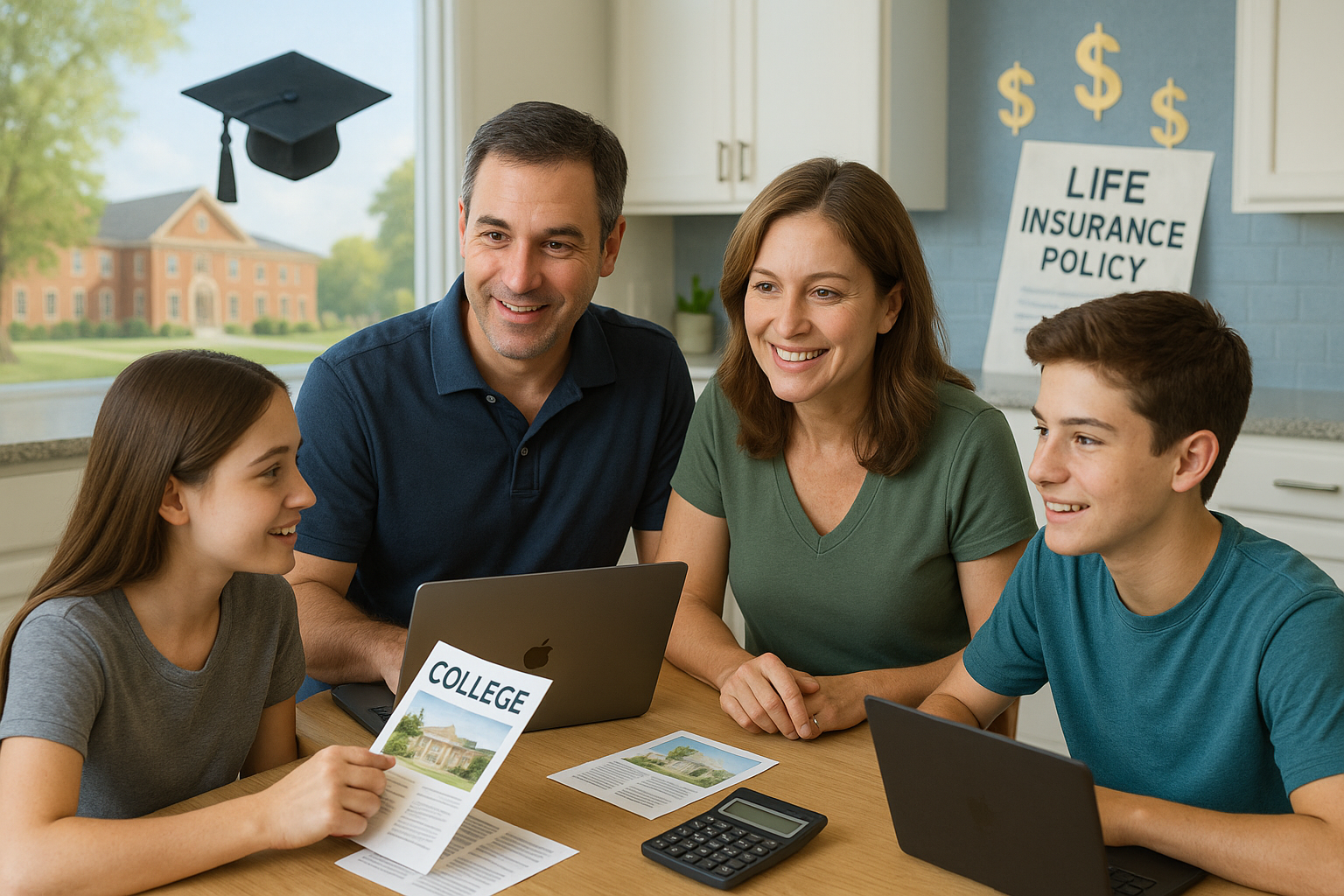

Why Life Insurance Is a Great Financial Tool

Life insurance is a flexible tool for planning your future. Here’s why it’s powerful:

- Use It for Anything: Unlike 529 plans, which are only for education, cash value can pay for a house, a business, or emergencies.

- Tax-Free Savings: Your cash value grows without taxes, and loans are often tax-free too. This saves you thousands compared to regular savings accounts.

- Family Protection: If something happens to you, the policy’s death benefit supports your family.

- Start Young, Save More: Young people pay lower premiums. A $150 monthly premium at age 25 could build $40,000 by age 40.

A 2023 LIMRA study showed families with life insurance feel 30% more financially secure. It’s like a savings account with a built-in safety net, perfect for students and parents.

Risks to Watch Out For

Life insurance isn’t perfect—it has some risks. Permanent policies cost more than term life, with premiums ranging from $100–$500 a month, depending on your age and coverage. If you miss payments, you could lose the policy and your savings. Borrowing from the cash value can also be tricky. If you don’t repay the loan, it might reduce your policy’s death benefit.

Some policies have fees, like 2–3% a year, which can shrink your cash value. Work with a trusted financial advisor to choose a policy that fits your budget. Researching carefully helps you avoid mistakes and make the most of your investment.

Choosing the Right Life Insurance Policy

Picking a life insurance policy is like choosing the right tool for a job—it needs to match your goals. Think about what you want: college funds, a house, or emergency savings? Permanent policies like whole life (steady growth) or universal life (flexible payments) are best for building cash value.

Look for trusted insurers like Northwestern Mutual or MassMutual—they get high ratings from AM Best. Compare premiums; a $200 monthly premium might work for a 25-year-old. Use online calculators to estimate growth—a $250,000 policy could build $20,000 in 10 years. A financial advisor can help you avoid bad deals.

Want more tips on mastering your finances? Check out our article on Why Schools Don’t Teach Money Management.

Getting Started with Life Insurance in 2025

Starting a life insurance policy is simple. First, research top insurers like Guardian or Prudential. Their websites offer free quotes. A 25-year-old might pay $120 a month for a $200,000 universal life policy. Use tools like calculators on NerdWallet or Insure.com to see how your savings could grow.

Talk to a financial advisor—they can explain terms and find a policy that fits your budget. Many offer free consultations. Start small if money’s tight—even $50 a month can build cash value over time. The key is to start now, as premiums get higher as you age.

Overcoming Barriers to Life Insurance

Some people think life insurance is too expensive or complicated. Don’t worry! You can find policies starting at $50 a month, especially if you’re young. Compare quotes to find one that fits your wallet. If the terms seem tricky, ask an advisor for help or check out free online resources.

Skeptical about insurance? That’s okay. Start with a small policy and see how it grows. Many colleges offer financial workshops to explain the basics. With the right plan, life insurance is a smart way to save for college and beyond.

Start exploring life insurance options now to save for college and beyond!

Conclusion: Secure Your Future Today

Life insurance is a powerful tool to pay for college, buy a home, or handle big expenses—without loans. Its cash value grows tax-free, and you can borrow it easily while keeping your family safe. Start young to lock in low rates and build savings faster. Don’t let college costs or unexpected bills hold you back.

Research policies, talk to an advisor, or watch Chadwick’s Experiences Full Interview with Esau Waters, Life Insurance Agent, to learn more. Take the first step today and build a brighter financial future!