Reading Changed My Life

People often ask why I spend so much time reading government reports, researching education policy, and interviewing experts instead of just repeating whatever is trending online.

Because reading lets you see what most people overlook.

Long before this year’s changes made national news, I was already researching how federal student loans worked. I wasn’t relying on social media clips. I wasn’t relying on political talking points from either side. I wanted to understand the actual system, not the headline version of it.

That research became the foundation for my books and for the conversations we have on Chadwick’s Experiences.

Why I Wrote My Books

I didn’t write my books because I dislike college. I earned two college degrees myself, and education changed my life.

I wrote them because I wanted students and parents to understand both sides of higher education: the opportunity, and the financial responsibility that comes with it.

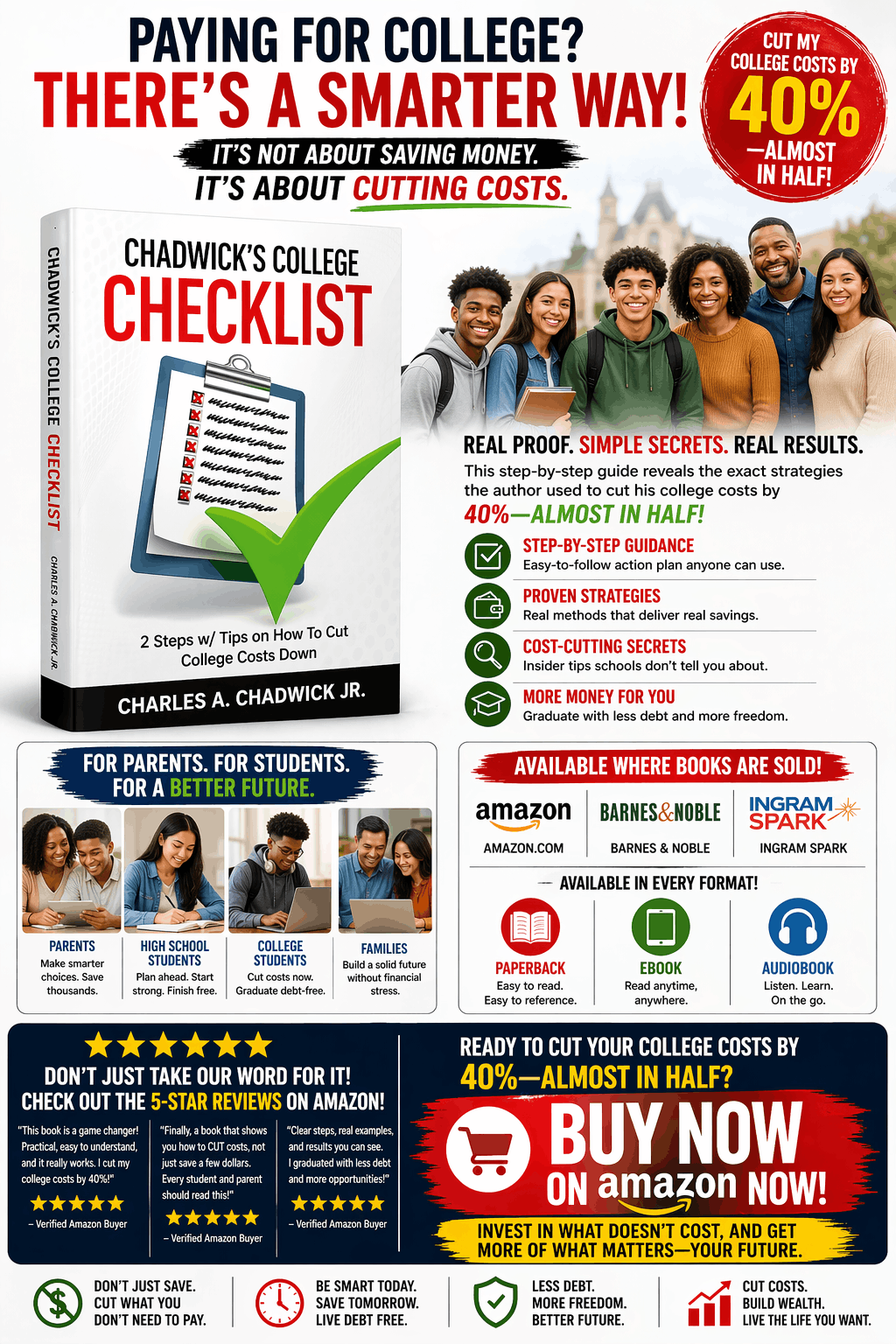

In my book, Chadwick’s College Checklist, I break down exactly how I cut my own college costs by 40% while still earning two degrees, without depending on outside financial help to bail me out. My books encourage readers to ask better questions before they ever borrow a dollar. Some of the topics include:

- Reducing college costs

- Understanding student loans

- Building financial literacy

- Exploring alternative career pathways

- Skilled trades and apprenticeships

- Entrepreneurship and side income

- Thinking long-term instead of emotionally

My goal has never been to tell everyone to skip college. My goal is to help people make smarter financial decisions, whatever path they choose.

College Debt or Skill Set?

One of the biggest questions I ask on Chadwick’s Experiences is this: is your career choice producing an education, or is it just creating debt?

For some people, college is absolutely the right investment. For others, apprenticeships, military service, certifications, skilled trades, or entrepreneurship provide a stronger financial return with a lot less debt attached. I’ve dug into this exact tradeoff in Student Loan Headache or Alternative Pathway, and the honest answer is that there isn’t one right path for everyone.

But there should always be one requirement: understand the financial consequences before you sign anything.

That starts with basic financial literacy, and it’s something most schools still don’t teach students before they graduate. If nobody ever showed you how interest, repayment terms, or loan servicers actually work, that’s not your fault. But it is your responsibility to learn it now, before you’re the one making six-figure decisions at eighteen years old.

Don’t Wait Until Graduation

One of my favorite sayings is this: don’t wait until graduation, use your imagination. It’s okay to make cash while you attend class.

While I was in college, I worked work-study jobs, sold items on eBay for other students, and looked for every way I could to earn income while I was still earning my degree. I go deeper into these kinds of income strategies in Make Cash While in Class: The Future of Work-Study, because waiting until after graduation to think about money is a habit that costs students real dollars every semester.

Some students go a step further and start building something of their own before they even walk across the stage. If that’s you, it’s worth reading Should Students Build a Business Before They Graduate? before you decide your only options are a part-time job or a bigger loan.

That experience taught me something valuable: your education should improve your finances. It shouldn’t be the reason you delay thinking about them.

My Mission Continues

The latest repayment changes are just another reminder that financial literacy isn’t optional. It’s required equipment.

Student loan policies will keep evolving. Repayment plans will keep changing. New administrations will keep introducing new ideas, and courts will keep ruling on them. But one thing never changes: knowledge is one of the best investments you’ll ever make, and nobody can take it away from you once you have it.

That’s why I continue writing books. That’s why I continue interviewing experts. That’s why Chadwick’s Experiences exists, built around a simple three-word mission I explain more in Learn, Earn, and Thrive.

In my book, The Pastor of the Student Loan Disaster, I use humor to tackle a subject most people find stressful, because sometimes you need to laugh your way through the numbers before they start making sense. It’s built for anyone who’s tired of scary headlines and wants a real plan instead.

If my work helps one student avoid unnecessary debt, if one parent asks one extra question before co-signing, if one family compares costs before borrowing, then every interview, every article, and every book has been worth it.

Why Financial Literacy Before College Isn’t a Nice-to-Have Anymore

Here’s the truth nobody likes to say out loud: not having financial knowledge is often worse than not having money. Money can be earned back. Bad financial decisions made from a place of confusion can follow you for twenty years.

This year proved that point better than any lecture could. Borrowers who didn’t know their SAVE plan was ending got caught off guard. Families who didn’t know Grad PLUS loans were disappearing made college choices based on numbers that no longer exist.

The lesson isn’t to be afraid of borrowing. The lesson is to never borrow blind.

Key Takeaways

- Student loan rules changed dramatically as of July 1, 2026, triggering the transition away from the SAVE plan and introducing new statutory caps on Parent PLUS loans.

- New borrowers now choose between only two repayment plans: the Tiered Standard Plan and the Repayment Assistance Plan (RAP).

- Borrowers impacted by the transition should actively review their official notices and check their status at StudentAid.gov rather than guessing.

- Policy will keep changing. The habit of asking financial questions before you borrow is the one thing that protects you no matter what changes next.

- Skilled trades, apprenticeships, and community college transfers remain strong alternatives worth comparing before you sign for a four-year loan.

Final Thoughts

Education is powerful. Financial education is just as important.

Before choosing a college, before signing loan paperwork, before assuming repayment plans will always stay the same, take the time to understand the numbers. Read. Ask questions. Compare your options.

Because the best student loan is often the one you never had to borrow in the first place.

About Charles A. Chadwick Jr.

Charles A. Chadwick Jr. is an Author, Speaker, and Visionary, and the host of Chadwick’s Experiences. He interviews experts, educators, skilled trades professionals, entrepreneurs, and financial leaders to help students and parents make informed educational and financial decisions. He reduced his own college costs by 40% while earning two degrees, without relying on loan forgiveness programs.

He is also the author of:

One Comment